Many people underestimate the significance of setting financial goals in their lives. By establishing clear and attainable financial objectives, you create a roadmap for your financial journey, allowing you to manage your resources more effectively. These goals motivate you to save, invest, and spend wisely, ultimately leading to greater financial security and fulfillment. Understanding the importance of setting these goals enables you to make informed decisions and stay focused on achieving your long-term dreams. In this post, we will explore why defining your financial goals is necessary for achieving your desired financial future.

Key Takeaways:

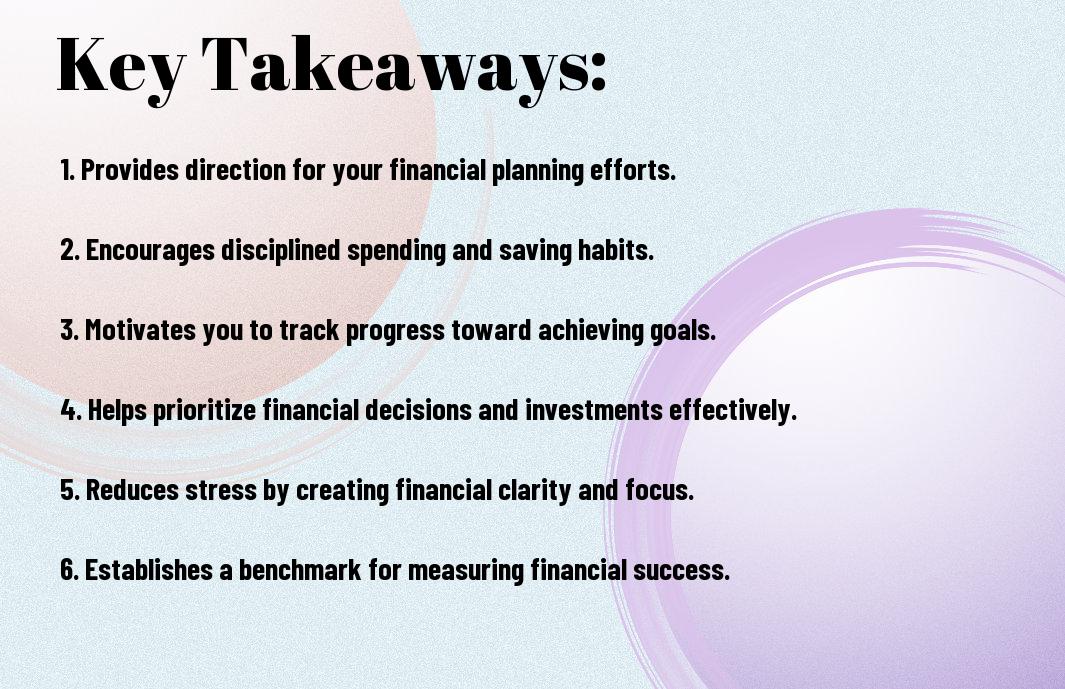

- Clarity: Setting financial goals provides a clear direction for where you want to go with your finances.

- Motivation: Specific goals help maintain your motivation and commitment to achieving better financial health.

- Measurement: Having set goals allows you to measure your progress and make adjustments to your financial plans as needed.

- Prioritization: Financial goals help you prioritize spending and saving, leading to more effective financial management.

- Accountability: Setting goals fosters a sense of accountability, encouraging you to take active steps towards achieving your desired financial outcomes.

Understanding Financial Goals

A financial goal is a target you set to achieve your desired financial outcomes. These objectives can vary widely, depending on your individual circumstances, aspirations, and timelines. By identifying and understanding your financial goals, you can create a structured plan that guides your financial decisions, enhancing your ability to achieve long-term wealth and security.

Definition of Financial Goals

Financial goals are specific objectives regarding your finances that you intend to achieve within a defined timeframe. These can range from saving for retirement, purchasing a home, or eliminating debt. By clearly defining these goals, you lay the groundwork for achieving financial stability and growth.

Types of Financial Goals

Various types of financial goals exist, each catering to different aspects of your life. These can primarily be categorized into short-term, medium-term, and long-term objectives. Here are some examples to consider:

- Saving for a vacation (short-term)

- Buying a car (medium-term)

- Building an emergency fund (short-term)

- Saving for a child’s college education (long-term)

- Preparing for retirement (long-term)

Assume that you want to make informed financial decisions, having clarity on these categories will significantly improve your planning process.

| Type of Financial Goal | Timeframe |

|---|---|

| Emergency Fund | Short-term |

| Vacation Savings | Short-term |

| Car Purchase | Medium-term |

| Home Purchase | Medium-term |

| Retirement Fund | Long-term |

To effectively pursue your financial goals, it’s crucial to categorize them appropriately based on the timeline for achievement. Keeping track of your goals will aid in refining your strategies and adapting them as necessary. Consider these types:

- Debt repayment (short-term)

- Saving for a wedding (medium-term)

- Investment in a business (medium-term)

- Financial independence (long-term)

- Achieving a net worth target (long-term)

Assume that you prioritize your goals correctly; this will help you focus your resources more effectively and improve your financial stability.

| Type of Financial Goal | Timeline |

|---|---|

| Debt Repayment | Short-term |

| Wedding Savings | Medium-term |

| Investment in Business | Medium-term |

| Financial Independence | Long-term |

| Net Worth Target | Long-term |

The Benefits of Setting Financial Goals

You can unlock numerous benefits by setting clear financial goals. These objectives provide a roadmap for your financial journey, allowing you to make informed decisions, prioritize spending, and achieve both short-term and long-term financial success. With well-defined goals, you can also track your progress, celebrate milestones, and ultimately cultivate a more secure financial future.

Enhanced Financial Awareness

Financial awareness is significantly heightened when you set goals. By defining what you want to achieve, you gain clarity on your current financial situation and identify the steps necessary to reach your targets. This heightened awareness leads to better budgeting, informed spending choices, and a deeper understanding of your financial habits, empowering you to make smarter decisions.

Motivation and Accountability

Benefits of setting financial goals include increased motivation and accountability in your financial endeavors. When you establish clear objectives, you create a sense of purpose that fuels your commitment to achieving them. This intrinsic motivation inspires you to stay focused and disciplined, while accountability mechanisms—such as sharing goals with friends or family—can keep you on track and provide support during challenging times.

Understanding the connection between motivation and accountability is crucial for reaching your financial goals. By sharing your aspirations with others, you create a support system that encourages you to follow through on your commitments. Regularly reviewing your progress can also foster a sense of responsibility, urging you to stay committed to your objectives. Consequently, these elements work together to enhance your financial discipline and resilience, ultimately guiding you toward lasting financial success.

The Goal-Setting Process

Your journey towards financial success begins with a well-structured goal-setting process. Establishing your financial goals methodically can help you stay focused and achieve desired outcomes. To enhance your understanding of this process, you can explore insights on Setting Financial Goals And Achieving Them. By taking the time to assess your priorities, evaluate your current situation, and define your objectives, you lay a solid foundation for financial well-being.

SMART Criteria for Goal Setting

Against the backdrop of goal-oriented strategies, the SMART criteria can guide you in creating effective financial goals. SMART stands for Specific, Measurable, Achievable, Relevant, and Time-bound. When you apply these principles, each goal gains clarity, making it easier to track progress and stay motivated throughout your financial journey.

Prioritizing Financial Goals

Goals must be prioritized to allocate resources effectively and address the most pressing needs first. By identifying which financial objectives hold the greatest importance to you, you can create a roadmap that directs your efforts and helps you make informed decisions.

The process of prioritizing financial goals involves evaluating their urgency and potential impact on your overall financial situation. You may start by listing all your goals, then classify them into short-term and long-term categories. This will help you focus on immediate objectives, such as building an emergency fund or paying off high-interest debt, while also keeping long-term aspirations, like retirement savings, in your sights. Prioritization empowers you to allocate your time and resources efficiently, guiding you towards achieving your financial aspirations.

Common Financial Goals

Unlike the general notion that all financial goals are the same, they can be distinctly categorized into short-term and long-term objectives, each tailored to your unique circumstances. Short-term goals often focus on immediate financial needs, while long-term goals help you build wealth over time, guiding your financial planning and spending habits.

Short-Term Goals

Goals in this category typically focus on achieving milestones within one to three years. This could include saving for a vacation, paying off credit card debt, or building an emergency fund. By setting these goals, you can create a pathway to enhance your financial stability quickly and effectively.

Long-Term Goals

Before entering into your financial journey, it’s important to outline your long-term goals, which generally span over five years and often include saving for retirement, buying a home, or funding your children’s education. These objectives require a strategic approach since they involve more significant financial commitments and investments.

With long-term goals, you are creating a vision for your future financial landscape. These goals encourage disciplined saving and investing, allowing you to accumulate wealth over time. Establishing clear long-term objectives can also help you withstand economic fluctuations, ensuring you remain focused on your overarching financial journey.

Overcoming Challenges in Goal Setting

Not every financial journey is smooth, and you may encounter challenges that hinder your progress. These hurdles can range from unexpected expenses to difficulties in maintaining motivation. Acknowledging that obstacles exist is the first step in overcoming them, allowing you to create a more resilient plan for achieving your goals.

Identifying Obstacles

Goal setting can be complicated when you’re unsure of the obstacles that lie ahead. To successfully navigate your financial path, it’s necessary to identify potential roadblocks that may disrupt your progress. This could include lack of funds, insufficient knowledge, or emotional barriers. Acknowledging these challenges early allows you to strategize and mitigate their impact.

Strategies for Staying on Track

Challenges are inevitable when pursuing your financial goals, but staying on track is achievable with the right strategies in place. Implementing a budget, regularly reviewing your progress, and adjusting your goals as needed can significantly enhance your likelihood of success. Additionally, consider enlisting the support of a mentor or a financial advisor to help you navigate complex situations.

A proactive approach will foster discipline and clarity in your quest for financial success. Setting up a routine for regular check-ins on your goals not only provides motivation but also allows you to adapt your strategies in real-time. Engaging with a support network can inspire you to stay focused and accountable. By embracing these strategies, you equip yourself to overcome difficulties and progress toward achieving your financial objectives.

Tracking Progress and Adjusting Goals

Once again, tracking your financial goals is important for ensuring you stay on the right path. Regularly reviewing your progress allows you to identify what’s working and what needs tweaking. This reflection gives you the opportunity to adjust your goals based on your financial journey, increasing the likelihood of achieving your desired outcomes.

Tools for Monitoring Financial Goals

Financial apps and spreadsheets are excellent resources that help you keep track of your progress. They can provide visual representations of your achievements and setbacks, making it easier to understand where you stand. By utilizing these tools, you can streamline your planning and develop a more focused approach to reaching your financial objectives.

When and How to Adjust Your Goals

On your financial journey, you might find that circumstances change, requiring you to adjust your goals accordingly. It’s vital to assess your situation periodically and shift your objectives to reflect new realities, whether it’s an unexpected expense, a pay raise, or a significant life change.

Considering the unpredictable nature of life, you should plan to review your financial goals at least biannually. Adjusting your goals involves looking at both your short-term and long-term aspirations. Determine whether your goals remain realistic and aligned with your current financial situation. Be open to refining your approach based on new information or experiences, ensuring that your financial journey remains dynamic and responsive to your needs.

Conclusion

So, understanding the importance of setting financial goals empowers you to take control of your financial future. By clearly defining what you want to achieve, you align your spending and saving habits with your aspirations. This strategic approach not only enhances your financial decision-making but also motivates you to stick to your plans. To probe deeper into the topic, explore this resource on The Importance of Setting Financial Goals.

Q: Why are financial goals important for personal growth?

A: Financial goals serve as a roadmap for individuals to achieve their aspirations and enhance their standard of living. By setting specific, measurable, achievable, relevant, and time-bound (SMART) goals, individuals can create a clear plan that outlines where they want to be financially. This clarity helps in prioritizing spending, saving, and investing, ultimately leading to a sense of control over one’s financial future.

Q: How can setting financial goals improve budgeting skills?

A: Establishing financial goals provides a foundation for effective budgeting. When individuals create goals, they can break them down into smaller, actionable steps. This process allows for the identification of necessary expenses and areas where costs can be cut. A well-defined budget aligned with personal financial goals encourages smarter spending habits and helps individuals stay on track toward reaching their financial milestones.

Q: What are some common types of financial goals people should consider?

A: Individuals can consider various types of financial goals, such as short-term, medium-term, and long-term objectives. Short-term goals may include saving for a vacation or an emergency fund, while medium-term goals could involve saving for a home or education expenses. Long-term goals typically focus on retirement savings or wealth accumulation. Setting a diverse range of goals allows individuals to build a balanced financial strategy that caters to immediate needs and future aspirations.